R语言-岭回归及lasso算法

2021-03-20 12:26

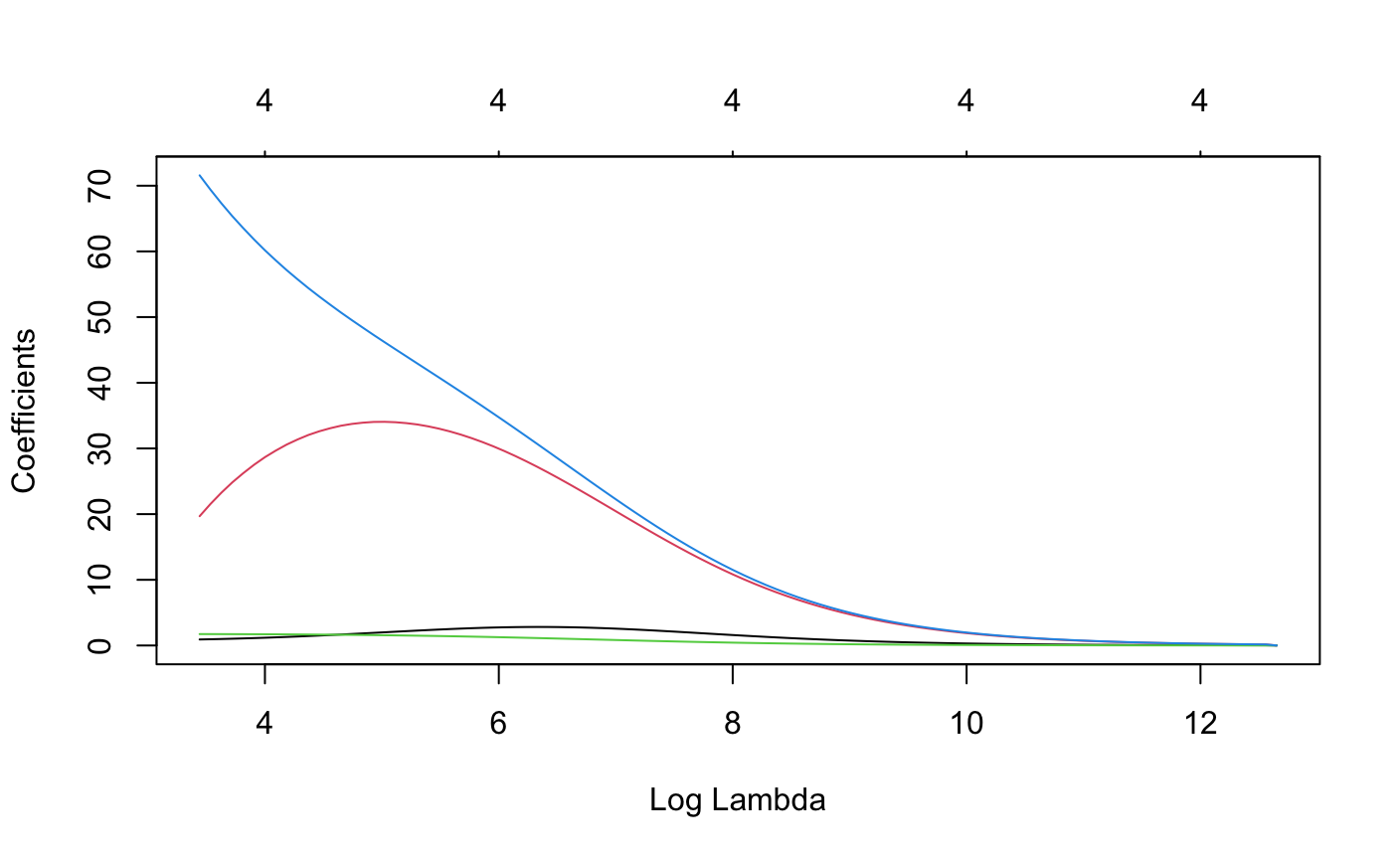

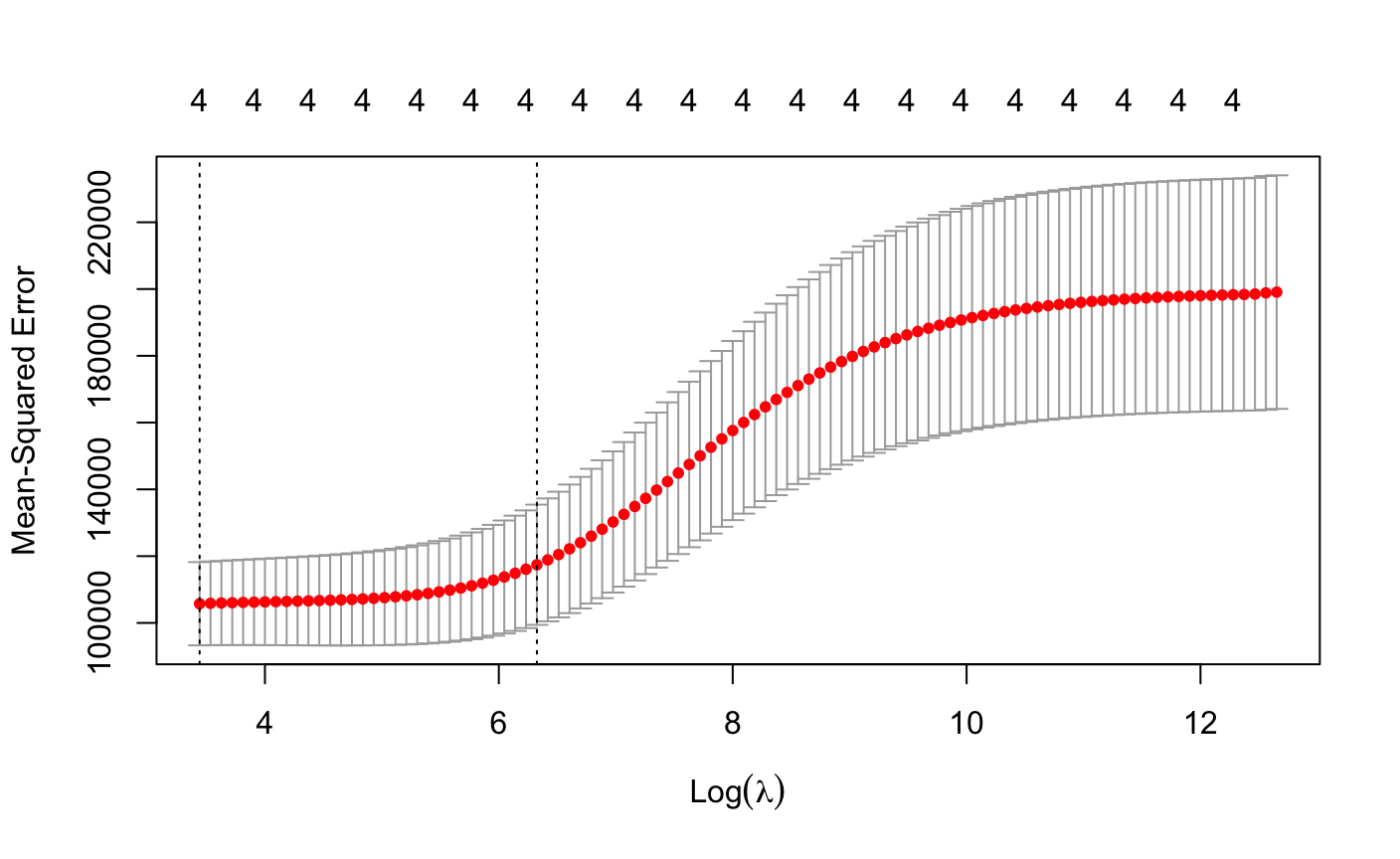

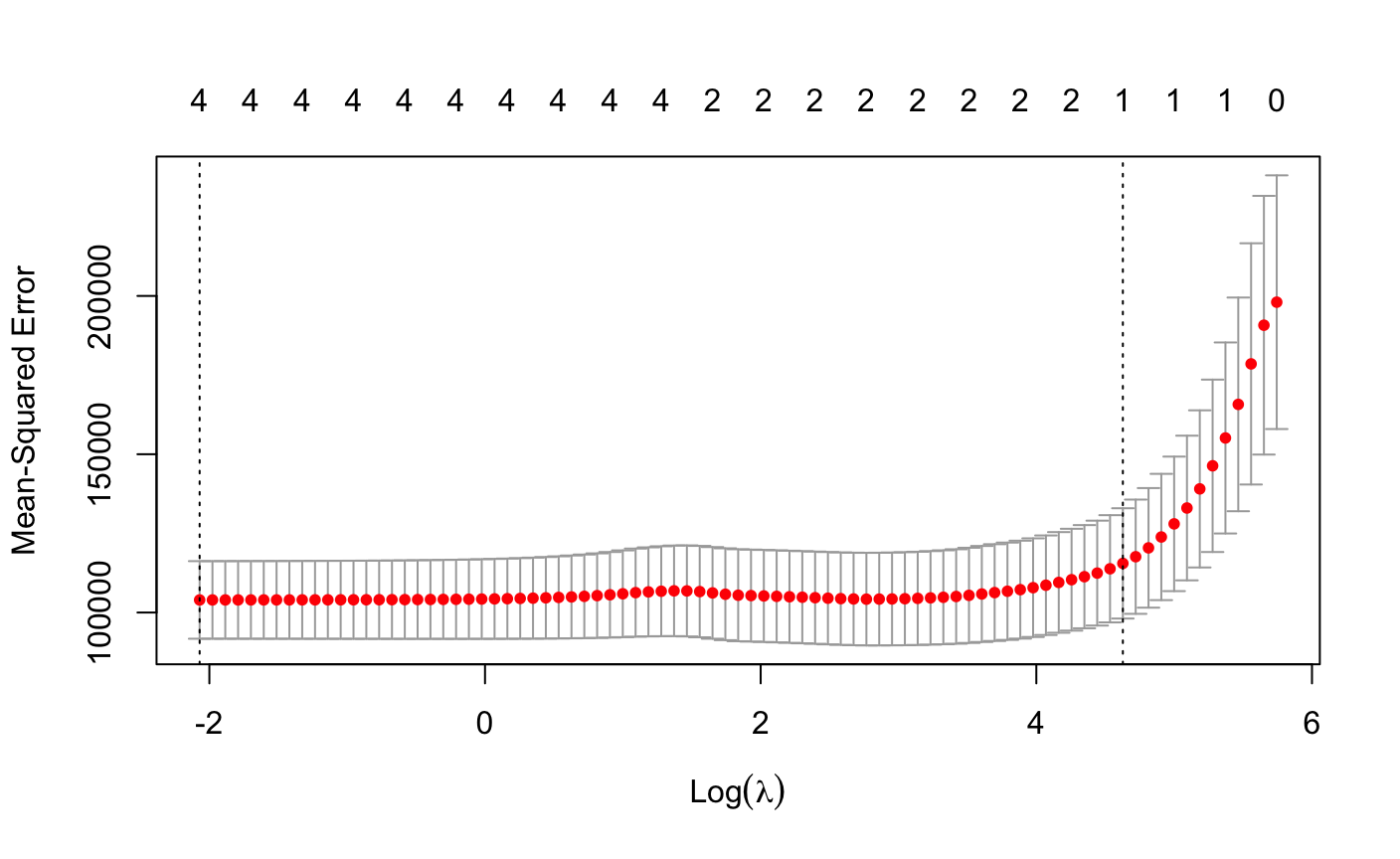

标签:lam let rgb complete min code gauss edit family 前文我们讲到线性回归建模会有共线性的问题,岭回归和lasso算法都能一定程度上消除共线性问题。 岭回归 我们可以看到这次模型的收入和支出是正相关了。 lasso算法 看模型数据,我们得知并没有解决income为负相关的情况,而且并没有筛选变量,那么我们尝试取lambda.1se*0.5的值 看结果,可知把一些变量删去了,消除共线性的问题,接下来我们看看lambda.1se的值 这次结果只留了一个变量,由此可知当lambda越大,变量保留的越少,一般我们在误差最小和一倍标准差内选择合适的λ。 R语言-岭回归及lasso算法 标签:lam let rgb complete min code gauss edit family 原文地址:https://www.cnblogs.com/ye20190812/p/13925000.html> #########正则化方法消除共线性

> ###岭回归

> ###glmnet只能处理矩阵

> library(glmnet)

> library(mice)

> creditcard_expcreditcard_exp[complete.cases(creditcard_exp),]

> x)])

> y])

> #看一下岭脊图

> r1"gaussian",alpha = 0)#alpha = 0表示岭回归,x,y不能有缺失值

> plot(r1,xvar="lambda")

> r1cv"gaussian",alpha=0,nfolds = 10)#用交叉验证得到lambda

> plot(r1cv)

> rimin"gaussian",alpha = 0,lambda = r1cv$lambda.min)#取误差平方和最小时的λ

> coef(rimin)

5 x 1 sparse Matrix of class "dgCMatrix"

s0

(Intercept) 106.5467017

Age 0.9156047

Income 19.6903291

dist_home_val 1.7357213

dist_avg_income 71.5765458

#####Lasson算法:有变量筛选功效

r1l"gaussian",alpha=1,nfolds = 10)

plot(r1l)

> r1l1"gaussian",alpha = 1,lambda = r1l$lambda.min)#取λ最小值看建模情况

> coef(r1l1)

5 x 1 sparse Matrix of class "dgCMatrix"

s0

(Intercept) -27.169039

Age 1.314711

Income -160.195837

dist_home_val 1.538823

dist_avg_income 255.395751

> r1l2"gaussian",alpha = 1,lambda = r1l$lambda.1se*0.5)#0.5倍标准误差的λ

> coef(r1l2)

5 x 1 sparse Matrix of class "dgCMatrix"

s0

(Intercept) 267.0510318

Age .

Income .

dist_home_val 0.6249539

dist_avg_income 83.6952253

1 > r1l3"gaussian",lambda = r1l$lambda.1se)

2 > coef(r1l3)

3 5 x 1 sparse Matrix of class "dgCMatrix"

4 s0

5 (Intercept) 432.00684

6 Age .

7 Income .

8 dist_home_val .

9 dist_avg_income 68.90894